Table of Contents

CPP Payment Dates and Guide

If you landed on this page, you may have searched on Google for CPP Payment dates. We’ve saved the time and outlined the important dates you should know.

The Canada Pension Plan, abbreviated as CPP, is a social insurance program offered to Canadians by the federal government. So long as you’re working in Canada and contributing to the plan, you’ll be eligible for CPP payments later in life when you retire. Since retirement planning is a crucial step later in life, you may have questions about how the CPP plan works, how much you’ll receive and when you can start collecting benefits. All of your questions can be answered below in this article.

What is CPP?

CPP stands for Canada Pension Plan and it’s a social insurance program that has played an important role in the retirement plan for many Canadians since it was introduced in 1995. CPP is a contributory program and is a taxable benefit that replaces part of your income when you retire.

Qualifying and Applying to CPP

In order to qualify for the CPP program, you must meet the following requirements:

- Be at least 60 years of age

- Made at least one valid contribution to CPP in the past (work you did in Canada or credits from a former spouse/common law partner at the end of the relationship)

If you qualify for CPP, you do not automatically receive payments. You need to apply to the program in advance of when you want your pension to start. You can apply for CPP payments with the Government of Canada below:

CPP retirement pension online application

CPP retirement pension paper application

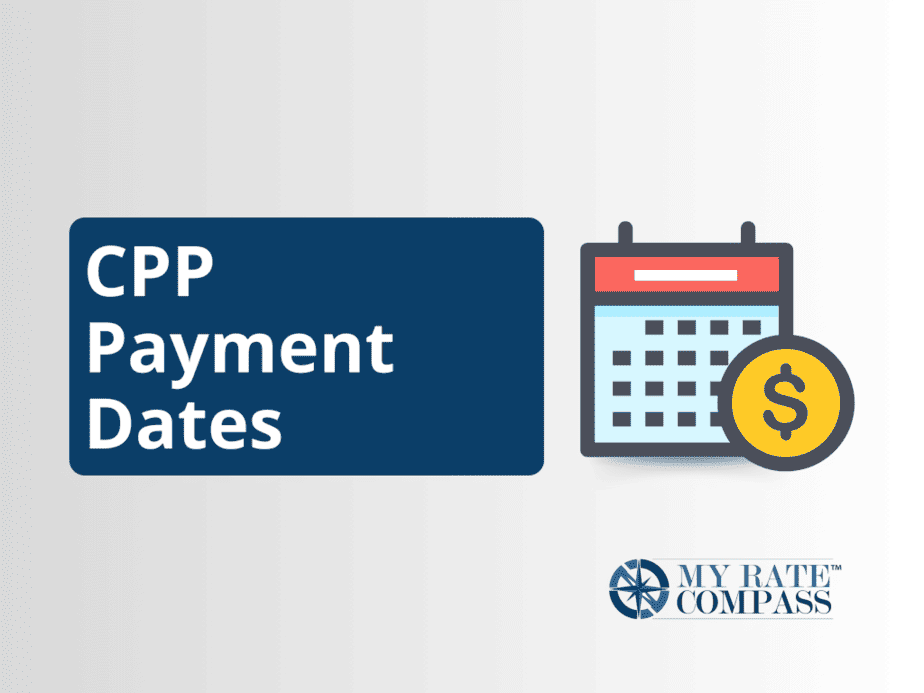

CPP payment dates 2024

The Canada pension payment dates for 2024 are below:

- January 29, 2024

- February 27, 2024

- March 26, 2024

- April 26, 2024

- May 29, 2024

- June 26, 2024

- July 29, 2024

- August 28, 2024

- September 25, 2024

- October 29, 2024

- November 27, 2024

- December 20, 2024

Average and Maximum CPP Monthly Payments

Even though you’re allowed to start your CPP payments at 60, there is an advantage to waiting until you’re 70. Every year that you claim CPP before your 65th birthday, your total amount is reduced by 0.6% which works out to be 7.2% per year. If you wait until you’re 70, your payments will increase by 0.7% for every month after your 65th birthday or 8.4% per year. After age 70, there is no increase or benefit to waiting to collect CPP. Most people start claiming CPP the month after their 65th birthday.

The amount of your CPP depends on how much you contributed throughout your life and how long you have paid into CPP. If you had periods with low earnings, there is a “general dropout” provision. In addition, if you were out of the workforce or worked part time for several years due to child care responsibilities, you can request a child rearing consideration.

Qualifying for the Maximum CPP Amount

To receive the maximum amount of CPP, you’d have to be making the maximum CPP contribution every year for many years. Every year, the federal government sets the year’s Maximum Pensionable Earnings (YMPE) which is the starting point for both CPP and pension contributions. The YMPE was $58,700 for 2020 and is $61,600 for 2021. To receive the maximum amount of CPP, you’d have to be making more than the YMPE for a significant number of years with no gaps in employment.

Specifically, in order to obtain the maximum amount of CPP, you must have done the following:

- Contributed to CPP for a minimum of 39 years of the 47 years from age 18 to 65

- Contributed the maximum amount to CPP for at least 39 years based on the YMPE

Every year has a different YMPE. To determine whether or not you contributed the maximum amount to CPP in previous years, check out this table.

Is CPP Taxable?

Yes, CPP retirement pension payments are considered taxable income. If you’re receiving CPP payments, you’re required to claim it on your income tax return and pay tax on the amounts you received. The amount of tax you pay on CPP payments depends on the other income you’re receiving and the tax bracket you fall under.

Additional CPP Benefits

There are more CPP benefits in addition to the retirement pension. Below is a summary of all the other CPP benefits available to Canadians.

- Disability Pension. Available for individuals already claiming CPP retirement pension and are disabled and therefore cannot work at any job on a regular basis.

- Post-retirement Disability Benefit. An extension of the disability pension that allows individuals who are not eligible for disability pension due to collection of CPP retirement pension for more than 15 months.

- Survivor’s Pension. Pension that is paid to a person who, at the time of death, is the legal common law partner or spouse of the deceased contributor.

- Children’s Benefit. CPP benefits provided to dependent children of disabled or deceased contributors. The child must be under age 18, or under age 25 at a full-time, recognized school.

- Death Benefit. A lump sum payment to an estate or beneficiary on behalf of a deceased CPP contributor.

The Canadian government has recently introduced something called CPP enhancement. Starting in 2019, CPP will slowly increase as a result of CPP enhancement. The new CPP enhancement will only apply to you if you are working and making contributions to CPP as of January 1, 2019 and onwards.

What Happens to CPP After You Die?

After you die, there are three potential options, additional CPP benefits you and your family could qualify for: death benefit, children’s benefit and survivor’s pension. Keep in mind that someone will have to apply for these benefits on your behalf after you pass.

What Happens to CPP If You Move Abroad?

If you move outside of Canada when you retire, CPP payments can be impacted. Unfortunately, there is not one rule that applies to all Canadians who move abroad in retirement. You may still be eligible for pension and benefits from Canada in addition to or in replacement of another country’s social benefits because of a social security agreement.

A social security agreement is an international agreement between another country and Canada that is in place to coordinate pension programs of the two countries for individuals who have worked or lived in both countries. These social security agreements can vary from country to country. To determine what kind of benefits you’ll be eligible for, check the details of the agreement that is applicable to you. Alternatively, you can contact a government representative to assist you.

CPP, Retirement and You

Many wonder whether CPP payments will be enough money for retirement. If you’re collecting the average CPP and standard Old Age Security (OAS) payments, then you’ll be receiving about $1,300 per month. If you live a very simple lifestyle, then it is possible to live off this amount of money. However, you will have to assess your lifestyle to determine how much money you need on a monthly basis to retire comfortably. Keep in mind there are other retirement tools out there such as a Registered Retirement Savings Program (RRSP).

CPP FAQs

Below are frequently asked questions about CPP payments and their respective answers.

Will CPP Amounts Increase in 2024?

Ever since the early 2000s, the rate of contribution has increased. Since contributions are increasing, the benefits will increase too. Furthermore, CPP benefits will increase as a result of the CPP enhancement program introduced in 2019.

What is the Maximum CPP for 2024?

The Year’s Maximum Pensionable Earnings (YMPE) is $68,500 for 2024. This is the maximum amount of money that you need to earn to contribute to the CPP plan. The maximum monthly amount you can possibly get paid if you start your pension at the age of 65 is $1,364.60.

Is Tax Deducted from CPP Payments?

The CPP retirement pension is considered taxable income. As a result, tax will be deducted from your CPP payments.

Can I Collect CPP While Working?

The standard age to collect CPP is 65, but you can start collecting payments as early as 60 or as late as 70. If you’re under these ages and still working, you cannot collect CPP. If you started working later and want to continue to work and contribute to CPP past age 60, you can. Even if you’re not retired by age 60, you can collect CPP payments.

What is the Best Age to Collect CPP?

There aren’t any golden rules in relation to when you should start collecting CPP, it depends on your financial situation. The most common time to begin collecting CPP is the month after you turn 65. The longer you wait to collect CPP pension, the more you’ll receive. However, waiting to collect CPP past 60 isn’t always the most optimal choice.

Before making a decision on when to start collecting retirement benefits, consider the following factors:

- What is your expected lifespan?

- Do you need the money now?

- OAS clawback considerations

- Current income levels

- Plans to continue working

Can CPP Cover Funeral Expenses?

If the deceased individual is eligible for the death benefit, that CPP benefit can be used to cover funeral expenses. Keep in mind that the death benefit is $2,500 and is paid into the deceased individual’s estate or to a beneficiary.

Can I Collect My Deceased Spouse’s CPP?

You cannot collect a deceased spouse’s CPP, but the surviving spouse can apply for the survivor’s pension CPP benefit. The amount that is paid depends on how much was contributed to the plan, other pension benefits you’re receiving and your age.